机器学习:决策树和组合算法

前言

以下是课程作业总结

问题来源:数据科学/方匡南编著,北京:电子工业出版社9.7.1/9.7.2习题

问题1:决策树

请分析R中ISLR包中的OJ(橘汁销售)数据集。该数据集包含了1070个顾客购买橙汁的记录。

- 用summary()函数查看数据基本信息,按7:3的比例划分训练集和测试集。

1 2 3 4 5 6 7 8 9 10

# 导入ISLR包 library(ISLR) # 查看数据基本信息 summary(OJ) # 设置随机种子以确保可重复性 set.seed(2333) # 划分训练集和测试集 train_index <- sample(1:nrow(OJ), 0.7 * nrow(OJ)) train_data <- OJ[train_index, ] test_data <- OJ[-train_index, ]

- 将purchase作为响应变量,其余变量作为预测变量,对训练集建立一棵树。用summary函数查看树的输出信息、训练错误率及树的终端节点个数分别是多少。

1 2 3 4 5 6

# 导入tree包 library(tree) # 建立一棵树 tree_model <- tree(Purchase ~ ., data = train_data) # 查看树的输出信息 summary(tree_model)

可看到输出信息:

1 2 3 4 5 6 7

Classification tree: tree(formula = Purchase ~ ., data = train_data) Variables actually used in tree construction: [1] "LoyalCH" "PriceDiff" "StoreID" "ListPriceDiff" Number of terminal nodes: 8 Residual mean deviance: 0.7527 = 557.7 / 741 Misclassification error rate: 0.1749 = 131 / 749

训练错误率约为0.1749,树的终端节点个数为8.

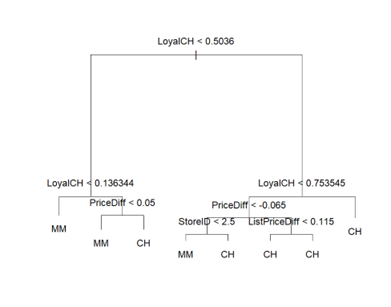

- 画出所建立的树并解释结果

1 2

plot(tree_model) text(tree_model, pretty=0)

输出图像:

- 预测测试数据的响应值,并计算测试错误率

1 2 3 4

# 预测测试数据的响应值 test_pred <- predict(tree_model, test_data,type="class") # 计算测试错误率 table(test_pred, test_data $ Purchase)

输出结果:

1 2 3 4 5

test_pred CH MM CH 176 55 MM 13 77 > (176+77)/(176+55+13+77) [1] 0.788162

结果显示,该模型预测准确率约为78.82%

- 对树进行剪枝,用cv.tree()函数在训练集上确定最优的树。并画出错误率对size的函数。则建立一棵含5个终端节点的树。

1 2 3 4 5

# 进行树的剪枝 cv_tree <- cv.tree(tree_model,FUN = prune.misclass) cv_tree # 画出错误率对size的函数图形 plot(cv_tree$size, cv_tree$dev, type = "b", xlab = "Size", ylab = "Deviance")

输出结果:

1 2 3 4 5 6 7 8 9 10

$size [1] 8 7 5 4 2 1 $dev [1] 141 140 160 164 165 285 $k [1] -Inf 0 3 4 5 134 $method [1] "misclass" attr(,"class") [1] "prune" "tree.sequence"

从上述数据和图像发现,当终端结点为7时,错误率最低,误差为140。

问题2:组合模型分析

- 根据ISLR包中的Default数据集:p=100,n=100.将数据集按照6:4的比例划分训练集和测试集,分别利用决策树、随机森林、Adaboost、Adaboost和logistic回归对训练集构建模型,利用测试集对所构建的模型进行测试。比较这几个模型的训练集预测准确率及测试集的预测准确率。

导入包和划分数据集:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

# 导入ISLR包 library(ISLR) # 设置随机种子以确保可重复性 set.seed(233) # 加载所需的包 library(tree) library(randomForest) library(gbm) library(xgboost) library(pROC) # 加载Default数据集 data(Default) # 划分训练集和测试集 train_index <- sample(1:nrow(Default), 0.6 * nrow(Default)) train_data <- Default[train_index, ] test_data <- Default[-train_index, ]

决策树:

1

2

3

4

5

6

7

# 决策树模型

tree_model <- tree(default ~ ., data = train_data)

tree_train_pred <- predict(tree_model, train_data,type="class")

tree_test_pred <- predict(tree_model, test_data,type="class")

table(tree_train_pred, train_data$default)

table(tree_test_pred, test_data$default)

随机森林

1

2

3

4

5

6

7

# 随机森林模型

rf_model <- randomForest(default ~ ., data = train_data, importance=TRUE)

rf_train_pred <- predict(rf_model, train_data, type="class")

rf_test_pred <- predict(rf_model, test_data, type="class")

table(rf_train_pred, train_data$default)

table(rf_test_pred, test_data$default)

Adaboost

对于Adaboost模型,先将非数值项编码为数字,然后我们取n.trees=5000和interaction.depth=4作限制,阈值取0.5,

代码:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

# 将非数值项转换为0或1

train.num <- train_data

test.num <- test_data

train.num$default<-as.numeric(train_data$default) - 1

train.num$student<-as.numeric(train_data$student) - 1

test.num$default<-as.numeric(test_data$default) - 1

test.num$student<-as.numeric(test_data$student) - 1

adaboost_model <- gbm(default ~ ., data = train.num, distribution = "adaboost",n.trees = 5000,interaction.depth = 4)

summary(adaboost_model)

adaboost_train_pred <- predict(adaboost_model, train.num, n.trees = 5000,type="response")

adaboost_train_pred <- ifelse(adaboost_train_pred > 0.5, 1, 0)

adaboost_test_pred <- predict(adaboost_model, test.num, n.trees = 5000,type="response")

adaboost_test_pred <- ifelse(adaboost_test_pred > 0.5, 1, 0)

table(adaboost_train_pred, train.num$default)

table(adaboost_test_pred, test.num$default)

XGboost

此处代码的计算过程应有误,因为ROC并不正常

1

2

3

4

5

6

7

8

9

10

11

12

# XGBoost模型

xgtrain_s <-Matrix::sparse.model.matrix(default~.-1, data = train_data)

xgtest_s <-Matrix::sparse.model.matrix(default~.-1, data = test_data)

dtrain <- xgb.DMatrix(data = xgtrain_s,label = train_data$default)

dtest <- xgb.DMatrix(data = xgtest_s,label = test_data$default)

xgboost_model <- xgboost(data = dtrain, max.depth=10,min_child_weight=1,gamma=0.1,colsample_bytree=0.8,subsample=0.8,scale_pos_weight=1,eta=0.1,eval_metric="auc",nround=10000,silent=TRUE)

xgboost_train_pred <- predict(xgboost_model, dtrain)

xgboost_test_pred <- predict(xgboost_model, dtest)

table(as.numeric(xgboost_train_pred > 0.5), train_data$default)

table(as.numeric(xgboost_test_pred > 0.5), test_data$default)

logistic回归

1

2

3

4

5

6

7

8

# Logistic回归模型

logistic_model <- glm(default ~ ., data = train_data, family = "binomial")

logistic_train_pred <- predict(logistic_model, train_data, type = "response")

logistic_test_pred <- predict(logistic_model, test_data, type = "response")

logistic_train_pred <- ifelse(logistic_train_pred > 0.5, 1, 0)

logistic_test_pred <- ifelse(logistic_test_pred > 0.5, 1, 0)

table(logistic_train_pred, train_data$default)

table(logistic_test_pred, test_data$default)

利用ROC曲线比较模型的好坏,并计算模型的AUC值。

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

train_accuracy <- function(pred, actual) {

mean(pred == actual)

}

test_accuracy <- function(pred, actual) {

mean(pred == actual)

}

# 计算各模型的训练集和测试集预测准确率

# 计算各模型的ROC曲线和AUC值

train_accuracy <- function(pred, actual) {

mean(pred == actual)

}

test_accuracy <- function(pred, actual) {

mean(pred == actual)

}

train.num$default

models <- c("决策树", "随机森林", "Adaboost", "XGBoost", "Logistic回归")

train_acc <- c(train_accuracy(tree_train_pred, train_data$default),

train_accuracy(rf_train_pred, train_data$default),

train_accuracy(adaboost_train_pred, train.num$default),

train_accuracy(as.numeric(xgboost_train_pred > 0.5), train.num$default),

train_accuracy(logistic_train_pred, train.num$default))

test_acc <- c(test_accuracy(tree_test_pred, test_data$default),

test_accuracy(rf_test_pred, test_data$default),

test_accuracy(adaboost_test_pred, test.num$default),

test_accuracy(as.numeric(xgboost_test_pred > 0.5), test.num$default),

test_accuracy(logistic_test_pred, test.num$default))

result <- data.frame(Model = models, Train_Accuracy = train_acc, Test_Accuracy = test_acc)

result

# auc

roc_curve <- roc(test_data$default, as.numeric(tree_test_pred))

auc_tree <- auc(roc_curve)

roc_curve <- roc(test_data$default, as.numeric(rf_test_pred))

auc_rf <- auc(roc_curve)

roc_curve <- roc(test_data$default, as.numeric(adaboost_test_pred))

auc_adaboost <- auc(roc_curve)

roc_curve <- roc(test_data$default, as.numeric(xgboost_test_pred))

auc_xgboost <- auc(roc_curve)

roc_curve <- roc(test_data$default, as.numeric(logistic_test_pred))

auc_logistic <- auc(roc_curve)

# 打印结果

auc_result <- data.frame(Model = models, AUC = c(auc_tree, auc_rf, auc_adaboost, auc_xgboost, auc_logistic))

auc_result

最后输出结果是:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

> result

Model Train_Accuracy Test_Accuracy

1 决策树 0.9733333 0.97250

2 随机森林 0.9763333 0.97150

3 Adaboost 1.0000000 0.96600

4 XGBoost 0.0340000 0.03225

5 Logistic回归 0.9740000 0.97200

> auc_result

Model AUC

1 决策树 0.6598199

2 随机森林 0.6218352

3 Adaboost 0.6826892

4 XGBoost 0.8246152

5 Logistic回归 0.6445743

不要问为什么XGboost的ROC值怎么奇怪,因为就是错的

思考如何选择最优模型来预测

从roc和auc值综合考虑,Adaboost模型最优。

本文由作者按照 CC BY 4.0 进行授权